The Bankruptcy and Insolvency Act (BIA) is the act respecting bankruptcy and insolvency in Canada.

The BIA is sometimes simply called the bankruptcy act, and it protects you and your rights, as well as the rights of the creditors, and gives the courts and trustees instructions on their duties, powers and responsibilities when helping a person file bankruptcy.

The BIA governs all Canadian bankruptcies, consumer and commercial proposals and receiverships, and the BIA also is responsible for governing the Office of the Superintendent of Bankruptcy (OSB).

The “Act” is provincial law and covers people in financial trouble with bankruptcy and proposal services.

The BIA covers laws regarding debts owing by the debtor.

If the debtor owes plenty of unsecured debts, a bankruptcy filing could be a way to get your fresh financial start.

Enacted in 1869, the first Canadian bankruptcy act was known as “An Act respecting Insolvency” and only covered traders.

It was not until 1919, with the Bankruptcy Act of 1919, until bankruptcy was available for all individuals, corporations, and other entities.

The Bankruptcy and Insolvency Act that we know today was not enacted until 1992.

In 1992, when the Act was renamed the BIA provisions for consumer proposals were made.

The Act was again updated in 1998 to deal with the discharge of student loan debt in insolvency.

The last update to the BIA went into force in 2009, which established the Wage Earner Protection Program, which allows compensation to employees of bankrupt companies or companies that were placed in receivership under the BIA.

The BIA also governs the Companies Creditors Arrangement Act (CCAA) in Canada.

If someone wants to make a proof of claim the Bankruptcy & Insolvency Act covers it.

The BIA covers insolvency law, how the insolvency proceedings work and how the stay of proceedings works for consumers who are unable to pay their debts as they become due.

Enacted in 1869, the first Canadian bankruptcy act was known as “An Act respecting Insolvency” and only covered traders.

It was not until 1919, with the Bankruptcy Act of 1919, until bankruptcy was available for all individuals, corporations, and other entities.

The Bankruptcy and Insolvency Act that we know today was not enacted until 1992.

In 1992, when the Act was renamed the BIA provisions for consumer proposals were made.

The Act was again updated in 1998 to deal with the discharge of student loan debt in insolvency.

The last update to the BIA went into force in 2009, which established the Wage Earner Protection Program, which allows compensation to employees of bankrupt companies or companies that were placed in receivership under the BIA.

The BIA also governs the Companies Creditors Arrangement Act (CCAA) in Canada.

If someone wants to make a proof of claim the Bankruptcy & Insolvency Act covers it.

The BIA covers insolvency law, how the insolvency proceedings work and how the stay of proceedings works for consumers who are unable to pay their debts as they become due.

Need Help Reviewing Your Financial Situation? Contact a Licensed Trustee for a Free Debt Relief Evaluation

Call 877-879-4770

or

History of the Bankruptcy and Insolvency Act

Enacted in 1869, the first Canadian bankruptcy act was known as “An Act respecting Insolvency” and only covered traders.

It was not until 1919, with the Bankruptcy Act of 1919, until bankruptcy was available for all individuals, corporations, and other entities.

The Bankruptcy and Insolvency Act that we know today was not enacted until 1992.

In 1992, when the Act was renamed the BIA provisions for consumer proposals were made.

The Act was again updated in 1998 to deal with the discharge of student loan debt in insolvency.

The last update to the BIA went into force in 2009, which established the Wage Earner Protection Program, which allows compensation to employees of bankrupt companies or companies that were placed in receivership under the BIA.

The BIA also governs the Companies Creditors Arrangement Act (CCAA) in Canada.

If someone wants to make a proof of claim the Bankruptcy & Insolvency Act covers it.

The BIA covers insolvency law, how the insolvency proceedings work and how the stay of proceedings works for consumers who are unable to pay their debts as they become due.

Enacted in 1869, the first Canadian bankruptcy act was known as “An Act respecting Insolvency” and only covered traders.

It was not until 1919, with the Bankruptcy Act of 1919, until bankruptcy was available for all individuals, corporations, and other entities.

The Bankruptcy and Insolvency Act that we know today was not enacted until 1992.

In 1992, when the Act was renamed the BIA provisions for consumer proposals were made.

The Act was again updated in 1998 to deal with the discharge of student loan debt in insolvency.

The last update to the BIA went into force in 2009, which established the Wage Earner Protection Program, which allows compensation to employees of bankrupt companies or companies that were placed in receivership under the BIA.

The BIA also governs the Companies Creditors Arrangement Act (CCAA) in Canada.

If someone wants to make a proof of claim the Bankruptcy & Insolvency Act covers it.

The BIA covers insolvency law, how the insolvency proceedings work and how the stay of proceedings works for consumers who are unable to pay their debts as they become due.

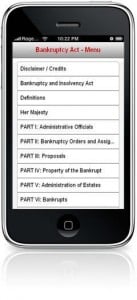

What Parts of the BIA are There?

The BIA is broken down into 14 main parts.

Part 1: Administrative Officials Lays out the responsibilities of the Licensed Insolvency Trustee (bankruptcy trustee), the official receivers and the Superintendent of Bankruptcy. Part 2: Bankruptcy Orders and Assignments This part of the Act lays out the Acts of bankruptcy and how to claim bankruptcy. Part 3: Proposals Part 3 of the BIA relates to proposals, including informal and formal consumer proposals. This third part of the Act lays out the roles of the trustee (consumer proposal administrator) and the consumer (you). Part 4: Property of the Bankrupt This part lays out how property is dealt with when going bankrupt. Non-exempt property and the bankruptcy exemptions. Part 5: Administration of Estates The handling of your estate (an estate is your assets and money) by trustees and your creditors. Part 6: Bankrupts The rights, duties, and responsibilities of a bankrupt. This part of the Act also lists how the bankruptcy law will help you. Part 7: Courts and Procedures This part of the BIA lays out the duties and roles of the court, including court orders. Part 8: BIA Offences The penalties for not following the rules of the BIA. Part 9: Miscellaneous Provisions This part of the BIA is for regulations and rules that do not fit in any other category. Part 10: Orderly Payment of Debts An orderly payment of debts is a bankruptcy alternative available in some provinces. Part 11: Secured Creditors and Receivers Secured debts are treated differently in bankruptcy so this part of the Act lists how property of secured creditors is handled. Part 12: Security Firm Bankruptcies This part of the Act gives instructions on how to deal with security firms in bankruptcies. Part 13: International Insolvencies This part deals with international insolvency filings. Part 14 General Rules Rules on aspects of the bankruptcy process.Need Help Reviewing Your Financial Situation? Contact a Licensed Trustee for a Free Debt Relief Evaluation

Call 877-879-4770

or